It'll be years before Americans get used to higher prices — and politicians can't just wait it out

Consumers will eventually adjust, but in the meantime, they'll keep punishing leaders who don't act

Strength In Numbers is a reader-supported publication. Paying members get articles like my weekly Deep Dive (co-written this week with David Nir of The Downballot) and access to polling crosstabs and additional premium posts. If you want more data-driven political journalism like this, join our community today as a paying subscriber.

Responding to Strength In Numbers’ recent work arguing that attitudes about the economy have sunk to record lows because Americans remain upset about prices that seem too high, Paul Krugman observed that “if nostalgia for past prices was the whole story, we would expect consumer sentiment to gradually improve as the ‘good old days’ of low prices recede further into memory.”

Krugman is right: Memories of the days of lower prices should fade out over time. The problem is that not enough time has elapsed for this seeming golden age to lose its grip on the American psyche.

In fact, it could be many more years before that happens, even under the most optimistic scenarios. If Democrats want to avoid getting punished at the polls over high prices — as they were in 2024, and as Republicans have been ever since — they’ll need to enact bold policies to improve voters’ financial well-being once they’re back in power.

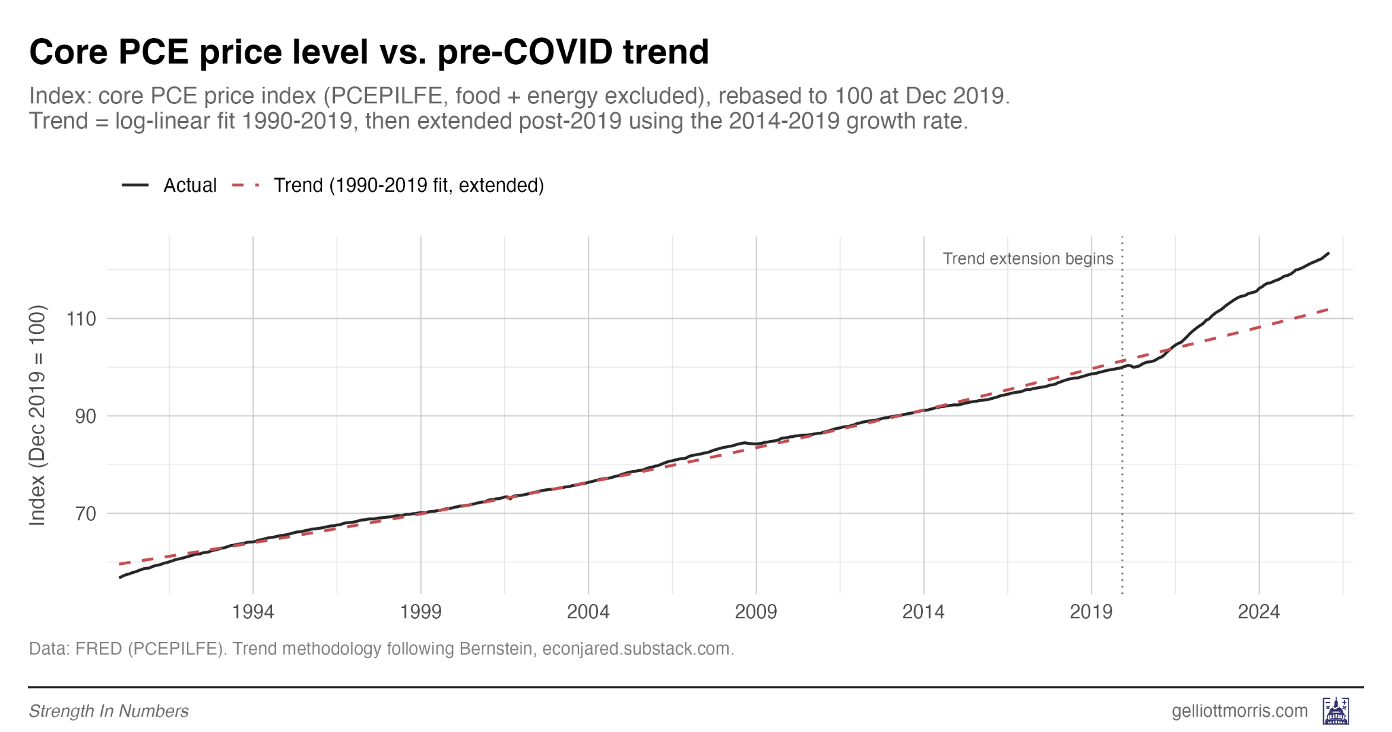

SIN’s new model for predicting American views on the economy rests on a metric called “excess inflation.” This measure, whose usefulness was first identified by economist Jared Bernstein, simply gauges how much higher prices are today compared to what consumers expected them to be after three decades of low inflation.

This is illustrated in the chart below. The dashed red line tells us where prices would have been had inflation in the United States never deviated from its pre-COVID level of about 2% per year. The solid dark line, on the other hand, shows us where prices actually stand today, following the spike in inflation in 2021-22 and higher-than-normal inflation ever since.

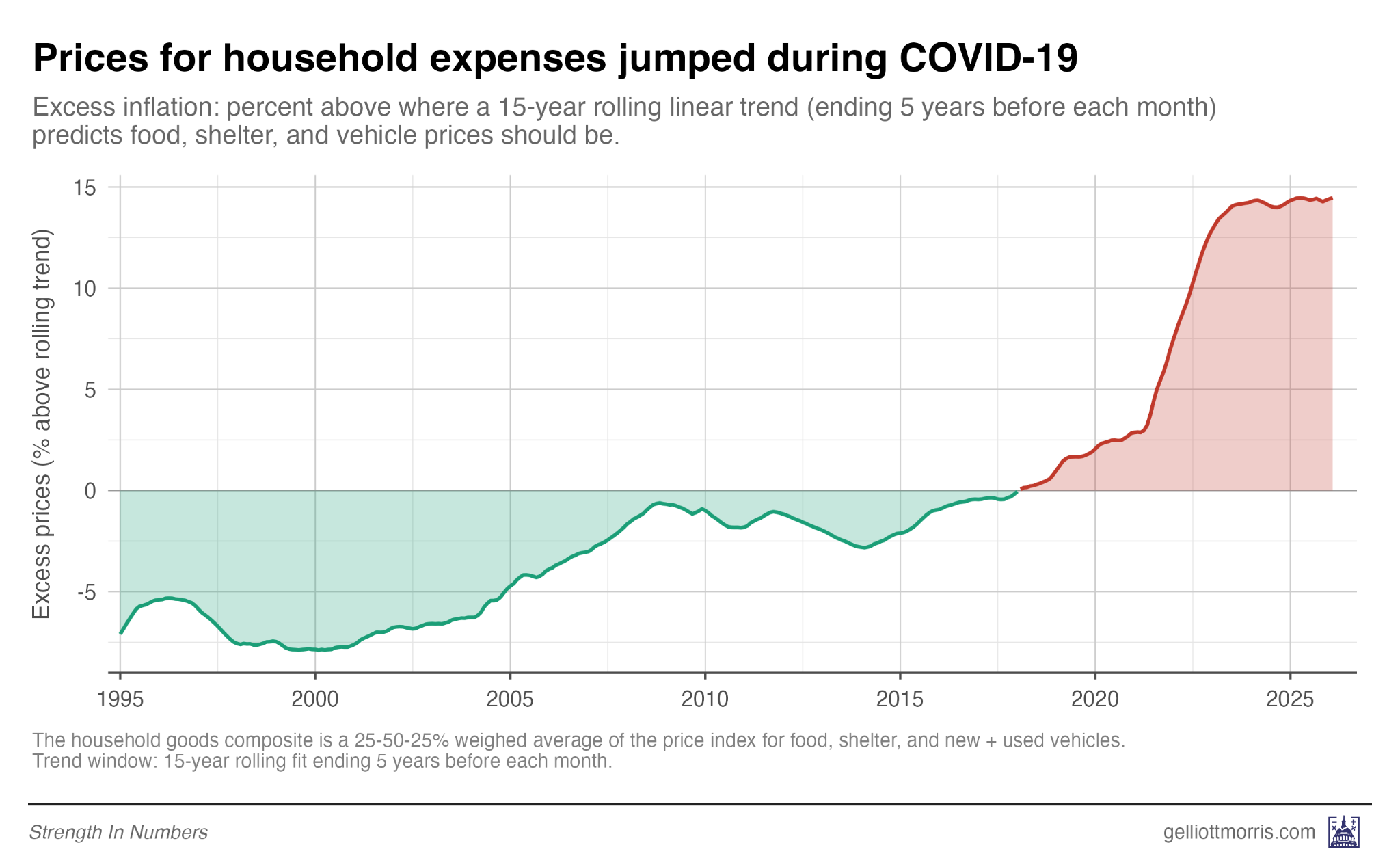

As a result, prices are now about 15% higher than Americans expected them to be. That’s “excess inflation,” which we see vividly in the next chart — the large red-shaded area below the trendline where it crosses the 0% horizontal axis in the middle of 2021.

This excess inflation, we’ve argued, has been the chief — though not only — cause of extremely sour feelings about the economy lately, and if you incorporate it into models that predict consumer sentiment, previously off-base estimates suddenly become much more accurate.1

When will consumers get used to high inflation?

Economists generally agree — and our model also implies — that consumers will eventually recalibrate their expectations for inflation such that prices that once seemed too high will start to feel normal. The question is, when?

Krugman has argued this recalibration should have — and perhaps has — happened by now.

“The big price surge began five years ago. That’s a long time. Do you remember what groceries cost in April 2021? I don’t, not really,” he wrote last month. “At some point one would expect people to recalibrate their expectations of what things ‘should’ cost. Yet the vibecession is if anything deepening with the passage of time.”

Our model suggests, however, that we haven’t yet reached that point, and won’t for quite some time.

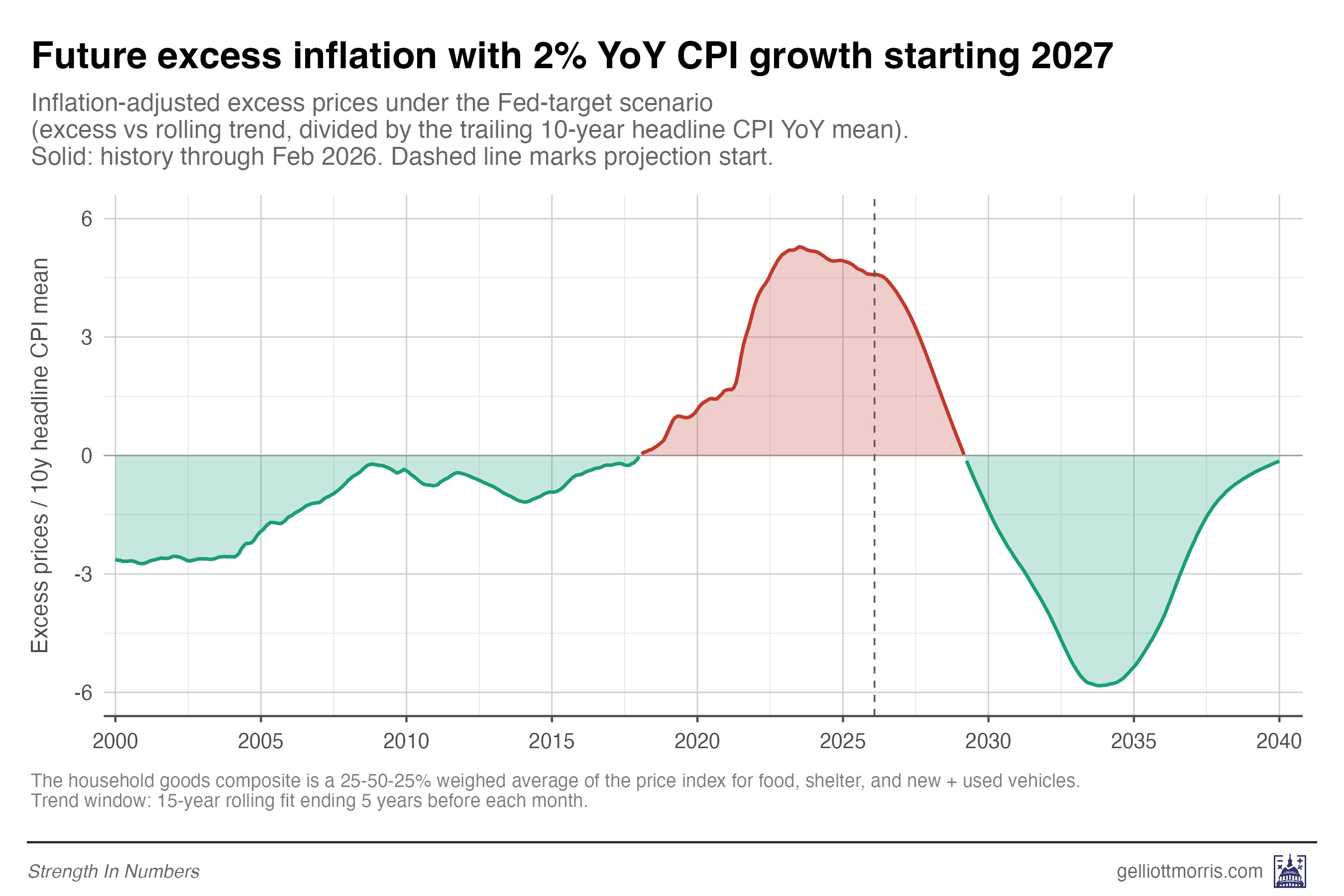

Exactly how long it will take for consumers to get used to this higher level of inflation depends on what happens with prices in the coming years. In an idealized best-case scenario, where inflation immediately returns to the Federal Reserve’s target of 2% per year and remains there, excess inflation wouldn’t return to zero for another three years — not until April of 2029:

In this scenario, excess inflation actually turns negative in late 2029 — and hits a trough in June of 2033 — because of the window the SIN model uses to predict what prices “should be” in a given month.

By the time we reach April 2029, the training data for the price model spans from April 2014 through April 2024. The model is therefore projecting what prices would have looked like in 2029 if the fast rate of inflation during Joe Biden’s presidency had held constant over the five years following his term in office. Since hypothetical inflation here is just 2%, “excess” prices are far below the benchmark. In 2034, it’s morning in America again!

We know that such a scenario is implausible, though, because inflation has remained above that 2% target ever since the pandemic, and because Donald Trump has pursued a set of policies — including tariffs, mass deportations, and war with Iran — that have only driven prices further upward.

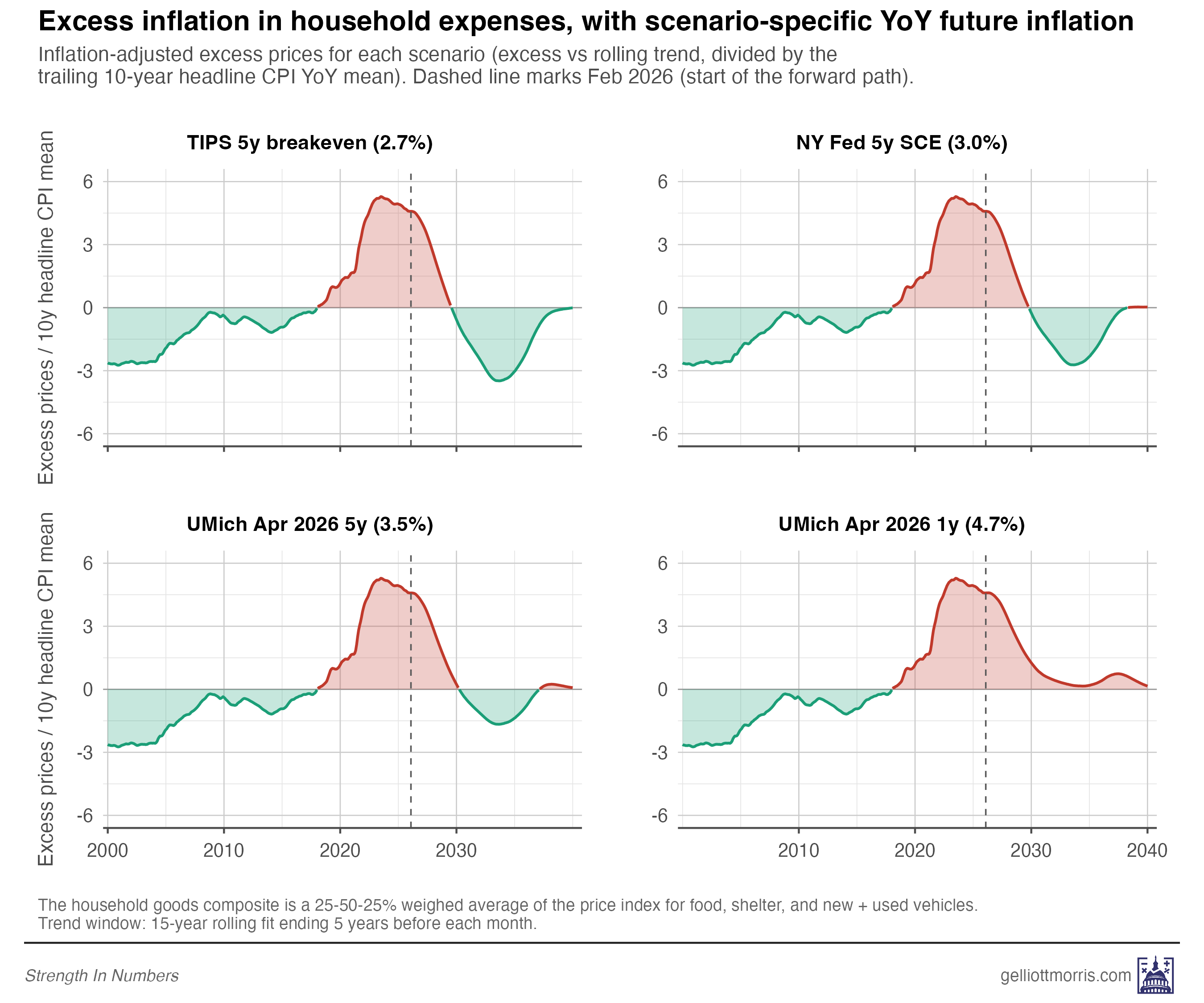

There are other scenarios we can analyze, though. The Fed actually attempts to measure expectations of future inflation in a variety of ways, though these often disagree with one another.

One metric, which is derived from the price investors are willing to pay for a type of bond known as Treasury inflation-protected securities, or TIPS, predicts that inflation over the next five years will average 2.7% per year. This figure has been trending upward since the start of Trump’s Iran war, but if we rely on its current value, the disappearance of excess inflation wouldn’t happen until August 2029.

Both the Fed and the University of Michigan also survey ordinary Americans to learn about their expectations for inflation. These consumer surveys are typically more bearish than metrics like TIPS, and that’s very much the case today.

The Fed’s latest readout for the next five years places inflation at an annual rate of 3%. That, of course, pushes any recalibration even further — out to November of 2029. The University of Michigan’s April poll, meanwhile, is worse still, clocking in at 3.5% over the coming half-decade. At this rate, excess inflation wouldn’t vanish until April 2030.

Both surveys, by the way, have seen spikes lately, just as TIPS has. And shorter-term expectations are even grimmer. The University of Michigan’s respondents predict inflation over the next year to clock in at 4.7% — up from 3.8% in March, one of the largest one-month jumps in the survey’s history.

If that expectation proves accurate, then excess inflation wouldn’t disappear until some time after 2040, though it would come close to zero in April of 2033.

Each of these scenarios is shown below:

The problem could be even worse.